China Pine Nut Kernel Export Analysis Report: 2024

Writer: Ray@pinenut.net , Meihekou City Jinfeng Food Co., Ltd.

1. Annual Overview of 2024

China’s surged to 14,518 MT in 2024 (+24.5% YoY), the highest volume since 2017. This rebound marked a shift toward emerging markets and supply chain modernization. Key drivers included:

- Vietnam’s breakout growth: Imports exploded to 784 MT (+1,320% YoY), ranking Vietnam as China’s fourth-largest market for .

- Southern Europe’s revival: Italy (1,079 MT, +47.8% YoY) and Spain (654.5 MT, +13.3% YoY) reached decade highs.

- Cost stabilization: Global logistics normalized, reducing airfreight expenses by 18% YoY for .

2. Country-Specific Analysis of Pine Nut Kernel Exports

(A) Volume and Market Share Trends

| Country | 2024 Volume (MT) | YoY Change | Share (2024) | Key Trend (2016–2024) |

|---|---|---|---|---|

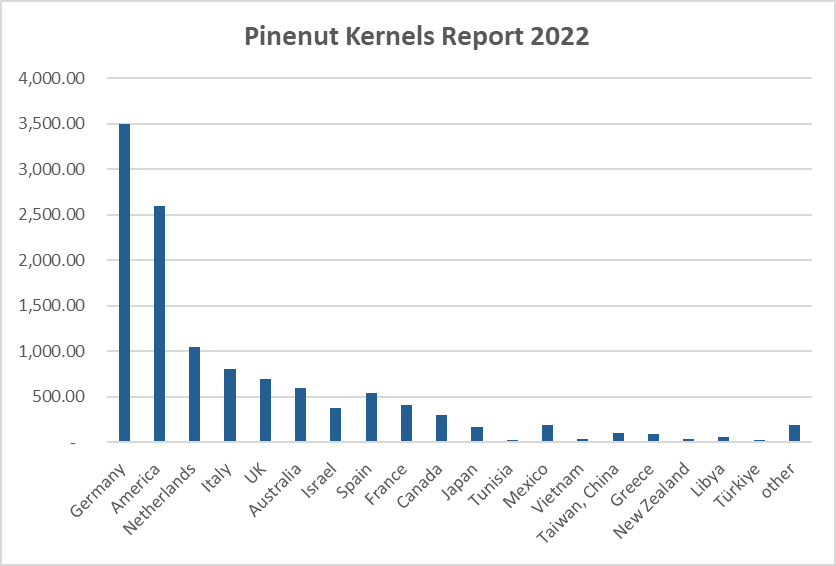

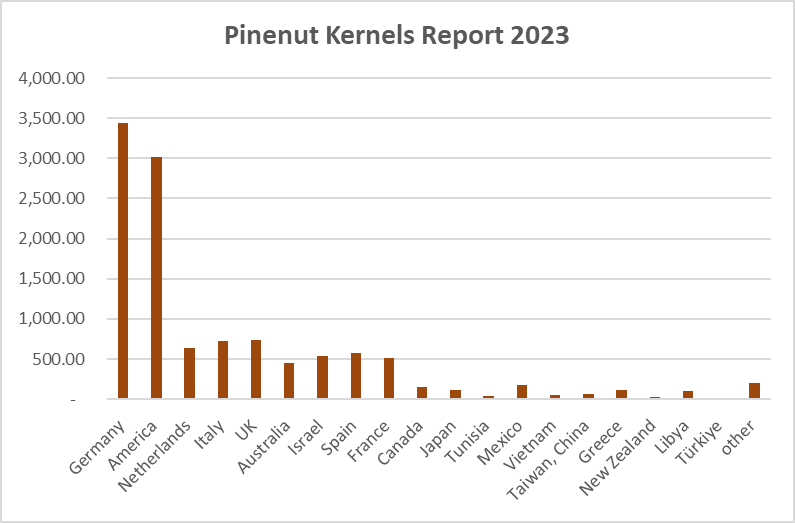

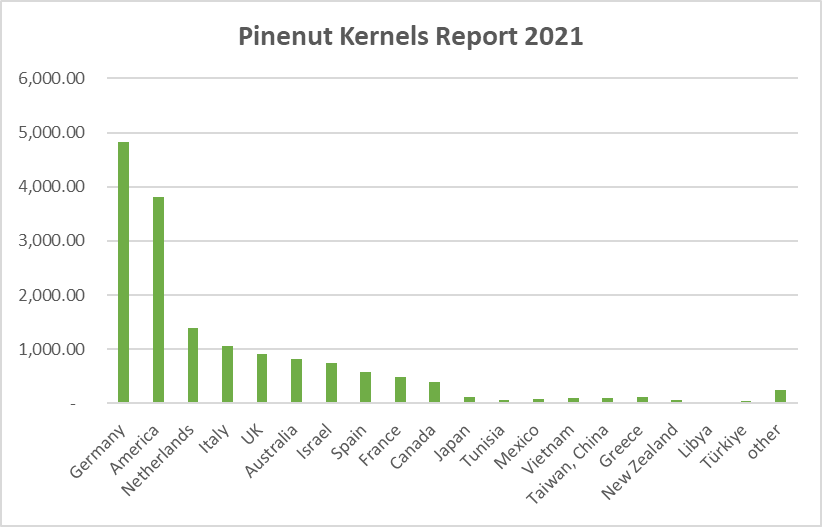

| Germany | 3,881.8 | +12.7% | 26.7% | Stabilized below 30% share for the first time since 2016. |

| United States | 3,033.5 | +0.8% | 20.9% | Tariff impacts fully absorbed, with stagnating demand. |

| Vietnam | 784.0 | +1,320% | 5.4% | Emerged as the largest ASEAN buyer of . |

| Spain | 654.5 | +13.3% | 4.5% | Doubled imports vs. 2016 (274 MT → 654 MT). |

(B) Regional Highlights

- European Union:

- Germany retained its top position with 3,882 MT (+12.7% YoY), while the Netherlands rebounded to 1,060 MT (+67% YoY).

- Greece collapsed to 51 MT (-53.6% YoY) amid debt crises, offset by Italy’s recovery.

- Asia-Pacific:

- Vietnam’s 784 MT dwarfed Australia’s 684 MT, redefining regional demand dynamics.

- Japan stagnated at 127 MT (+8% YoY), remaining a niche market.

- MENA:

- Libya solidified as a growth hub (112 MT, +6.6% YoY), while Israel rebounded to 640 MT (+19.7% YoY).

3. Long-Term Trends in Pine Nut Kernel Exports (2016–2024)

(A) Decadal Regional Rebalancing

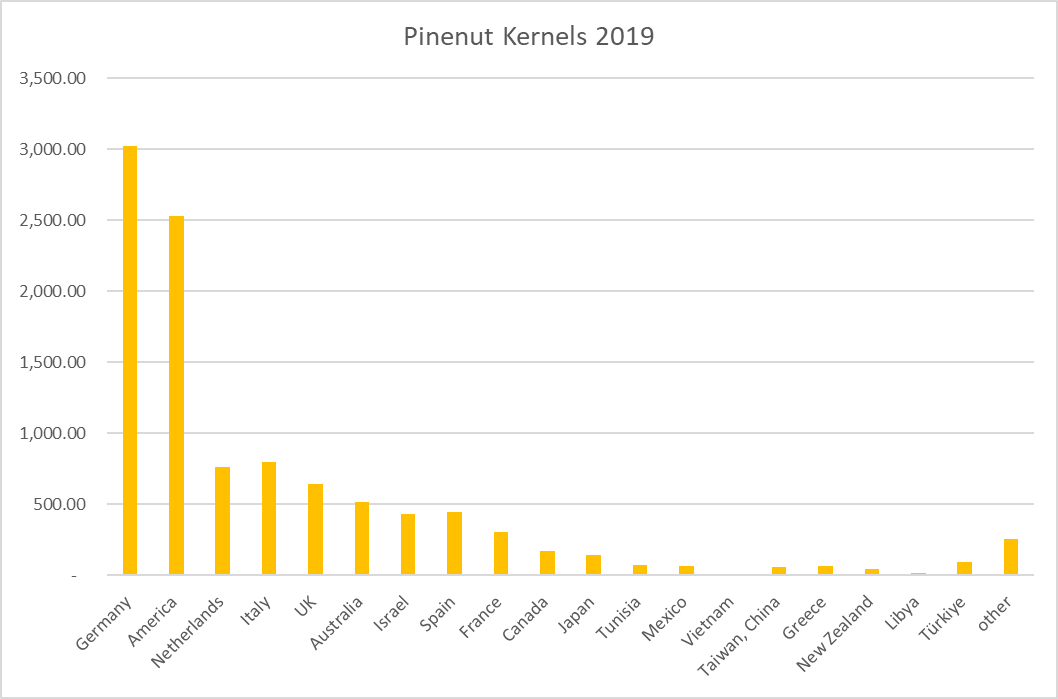

- Traditional markets: The EU & North America’s collective share fell to 57.8% (2024) from 72.1% (2016).

- Emerging markets: Asia-Pacific and MENA grew to 14.7% and 5.3% shares, respectively, up from 7.3% and 2.1% in 2016.

(B) Price and Competition Dynamics

- Average prices stabilized at **$8,200/MT** (+4% YoY), aligning with pre-pandemic trends.

- Pakistani and Russian undercut China’s prices by 12–15% in the EU.

(C) Logistic Innovations

- Rail Freight Expansion: 30% of to the EU used China-Europe rail routes, slashing delivery times.

4. Comparative Analysis with Historical Data (Pre-2024)

(A) Germany’s Enduring yet Diminished Role

- Despite a **-0.1% CAGR** (2016–2024), Germany retained dominance with 26.7% share (2024 vs. 27.1% in 2016).

- Contrasted with Spain’s **+13.1% CAGR** over the same period.

(B) Vietnam’s Historic Ascent

- Vietnam emerged as the fastest-growing buyer of , rising from 0.6 MT (2016) to 784 MT (2024) – a **+130.4% CAGR**.

(C) Southern Europe’s Revival

- Italy and Spain collectively imported 1,733 MT (2024), up **+81%** from 2016’s 958 MT, driven by bakery and confectionery sectors.

(D) MENA’s Divergent Paths

- Libya grew at a **+22.5% CAGR** (28 MT in 2016 → 112 MT in 2024), while Tunisia collapsed to 28 MT vs. 297 MT in 2016.