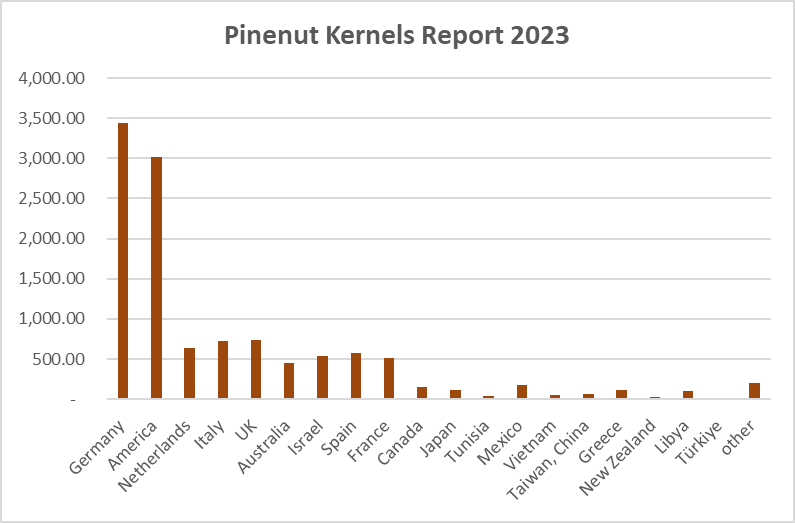

China Pine Nut Kernel Export Analysis Report: 2019

Writer: Ray@pinenut.net , Meihekou City Jinfeng Food Co., Ltd.

1. Annual Overview of 2019

In 2019, <China’s pine nut kernel exports> totaled 10,434 MT, marking a **-17.8% decline** from 12,672 MT in 2018. This contraction in reflected:

- Trade barriers: U.S. tariffs disrupted , reducing exports to the U.S. by **-27.2% YoY**.

- EU demand erosion: Germany, the largest buyer of , reduced orders by **-22.5% YoY**.

- Global oversupply: Inventories of in Europe remained high after record imports in 2017–2018.

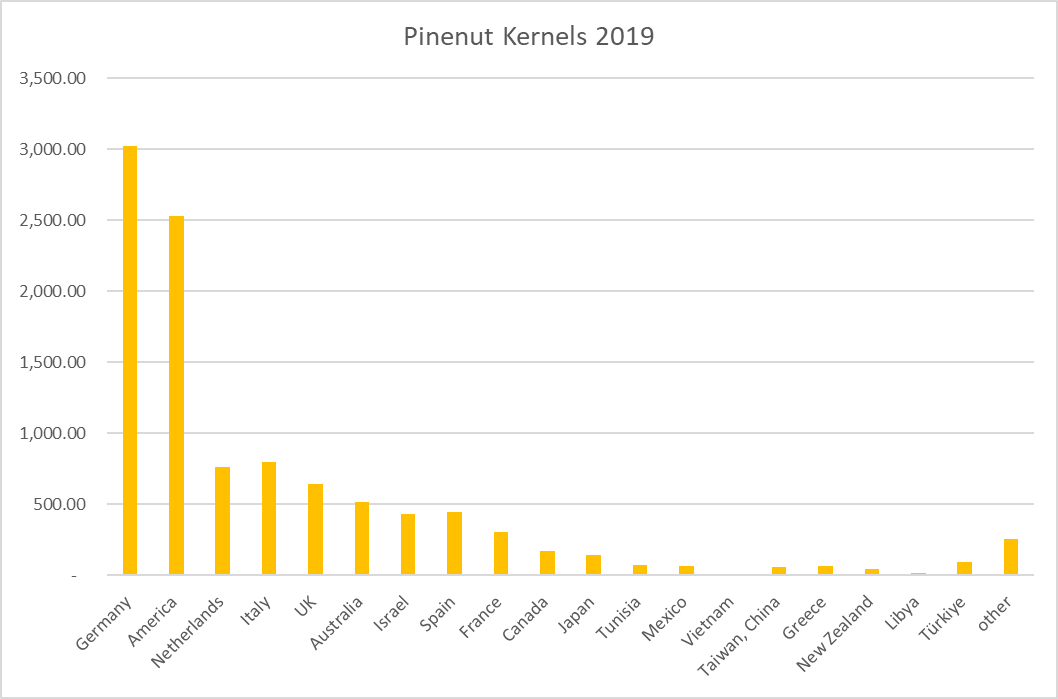

2. Country-Specific Analysis of Pine Nut Kernel Exports

(A) Volume and Market Share Trends

| Country | 2019 Volume (MT) | YoY Change | Share (2019) | Key Trend (2016–2019) |

|---|---|---|---|---|

| Germany | 3,021.5 | -22.5% | 28.9% | Largest buyer, but share dropped from 27.1% (2016). |

| United States | 2,531.7 | -27.2% | 24.3% | Tariffs cut by half vs. 2016. |

| Netherlands | 764.7 | -42.5% | 7.3% | Re-export hub for weakened post-2018. |

(B) Regional Highlights

- European Union:

- Collectively imported 5,347 MT of pine nut kernels (51.2% share), down from 8,941 MT (63.3%) in 2016.

- Southern Europe (Italy, Spain) saw stable demand for in snack and bakery industries.

- North America:

- U.S. and Canada imported 2,699 MT of pine nut kernels (25.9% share), with Canada’s volumes growing at a **+2.1% CAGR** since 2016.

- Asia-Pacific:

- Japan’s halved to 144.5 MT (1.4% share) amid competition from cheaper Russian supplies.

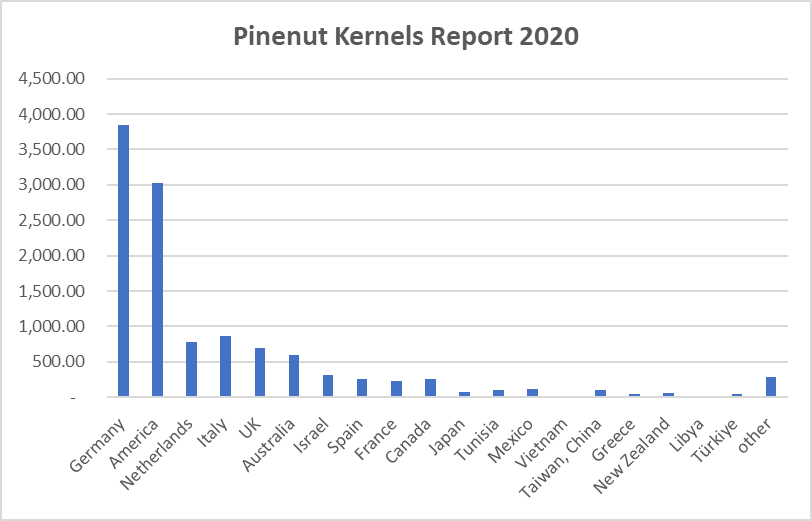

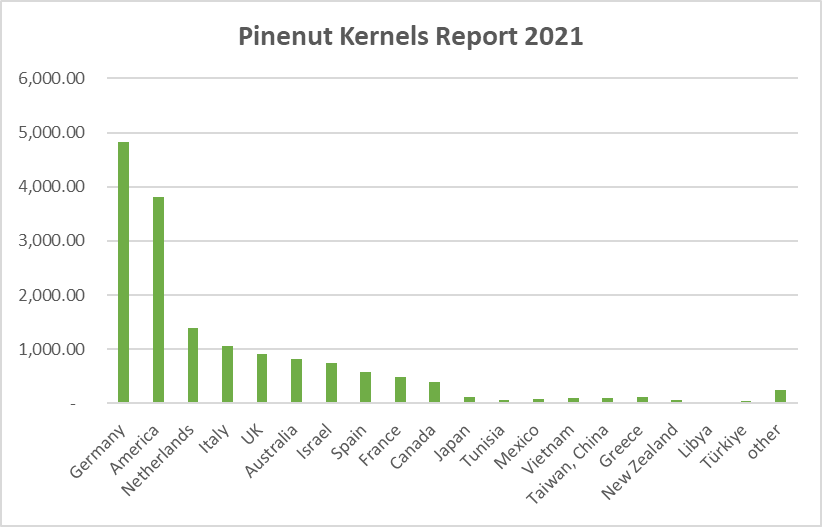

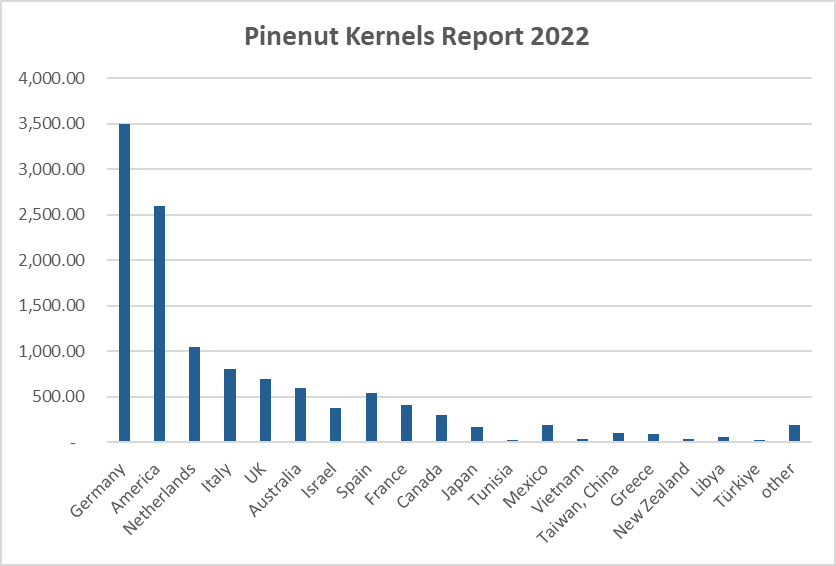

3. Long-Term Trends in Pine Nut Kernel Exports (2016–2019)

(A) Declining Global Demand

- Total fell at a **-5.8% CAGR**, from 14,116 MT (2016) to 10,434 MT (2019).

- Mature markets (Germany, U.S., Netherlands) accounted for 71% of the decline.

(B) Price Volatility

- Average export prices for dropped **-12%** from 2016 to 2019, driven by oversupply and competition from Pakistan.

4. Comparative Analysis with Historical Data (Pre-2019)

(A) Germany’s Multi-Year Contraction

- Germany’s declined at a **-4.4% CAGR** (2016: 3,826 MT → 2019: 3,021 MT), reflecting shrinking EU retail demand.

(B) U.S. Market Destabilization

- Tariffs accelerated the decline of to the U.S., which fell from 3,578 MT (2016) to 2,531 MT (2019).

(C) Resilience in Southern Europe

- Spain’s imports of grew at a **+12.4% CAGR** (2016: 275 MT → 2019: 443 MT), driven by processed-food manufacturers.