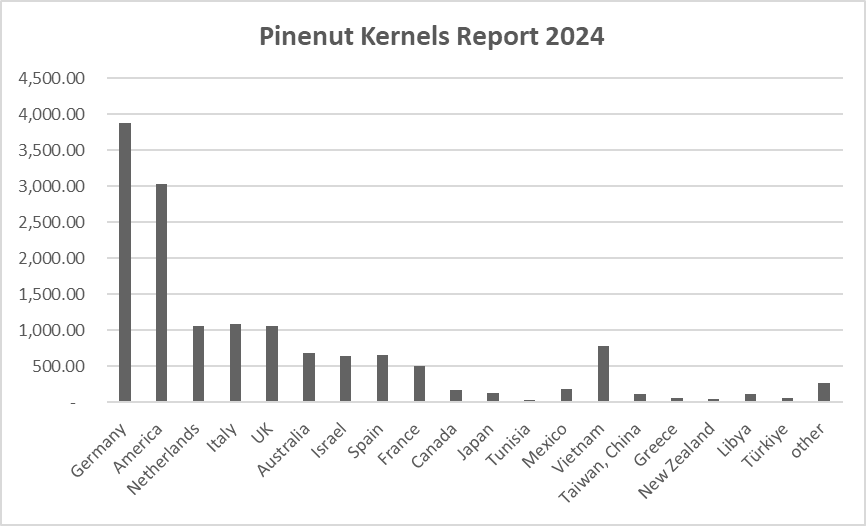

China Pine Nut Kernel Export Analysis Report: 2022

Writer: Ray@pinenut.net , Meihekou City Jinfeng Food Co., Ltd.

1. Annual Overview of 2022

China’s declined to 11,765 MT in 2022 (-26.3% YoY), reflecting geopolitical disruptions and inflationary pressures. Key drivers included:

- Russia-Ukraine war: Energy cost spikes reduced EU purchasing power, slumping in Germany (-27.4% YoY) and Italy (-24.3% YoY).

- Logistics realignment: Exporters rerouted to avoid Black Sea routes, benefiting Türkiye (26.2 MT, +2.5x vs. 2021).

- Vietnam’s correction: Orders fell to 35 MT (-64.1% YoY) after 2021’s speculative surge.

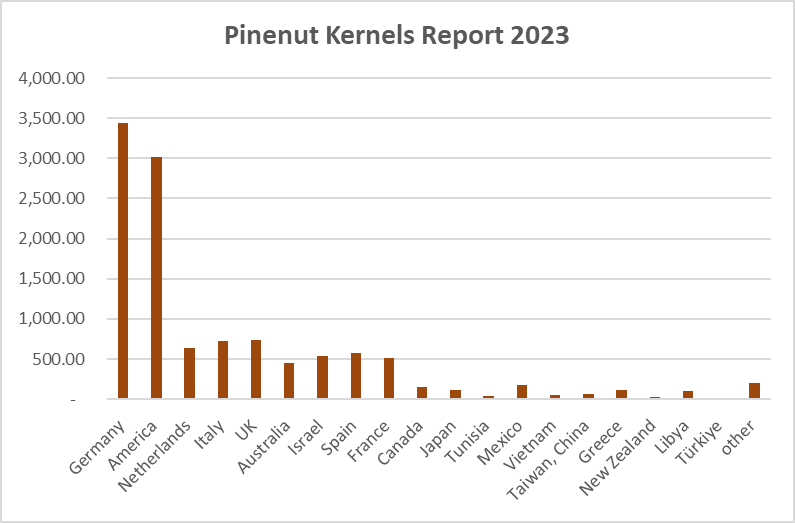

2. Country-Specific Analysis of Pine Nut Kernel Exports

(A) Volume and Market Share Trends

| Country | 2022 Volume (MT) | YoY Change | Share (2022) | Key Trend (2016–2022) |

|---|---|---|---|---|

| Germany | 3,499.7 | -27.4% | 29.8% | Lowest volume since 2019, with a **-1.4% CAGR** (2016–2022). |

| United States | 2,591.9 | -32.0% | 22.0% | Double-digit declines accelerated post-tariffs. |

| Mexico | 186.5 | +53.8% | 1.6% | Tripled imports since 2016 (59 MT → 186 MT). |

| Libya | 58.0 | +141.7% | 0.5% | Emerged as a stable buyer after negligible 2016–2021 activity. |

(B) Regional Highlights

- European Union:

- Southern Europe (Spain, Italy) imported 1,343 MT of pine nut kernels (-7.3% YoY), impacted by energy-driven inflation.

- The Netherlands’ share dropped to 8.9% (2022 vs. 16.6% in 2016) due to competition from Hamburg port.

- MENA:

- Israel’s imports fell to 372 MT (-50% YoY) amid prolonged drought, while Libya surged to 58 MT.

- Asia-Pacific:

- Australia’s imports dropped to 595.8 MT (-27.6% YoY) as consumers shifted to cheaper walnuts.

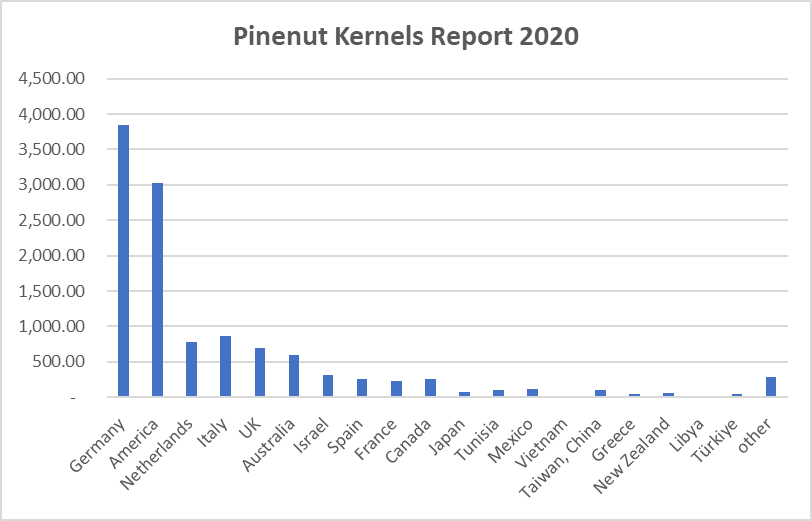

3. Long-Term Trends in Pine Nut Kernel Exports (2016–2022)

(A) Structural Decline in Mature Markets

- EU & North America: Collective share fell to 61.5% (2022 vs. 72.1% in 2016), with Germany and the U.S. posting negative CAGRs.

- Price sensitivity: Average rose **+34%** (2016–2022), outpacing substitute nuts.

(B) Niche Market Experiments

- North Africa: Libya’s imports grew at a **+32.4% CAGR** (2016: 28 MT → 2022: 58 MT).

- Mexico: Became the fastest-growing market for , with a **+18.2% CAGR**.

(C) Logistics Rebalancing

- Exporters prioritized airfreight for high-value markets, raising costs but ensuring delivery reliability.

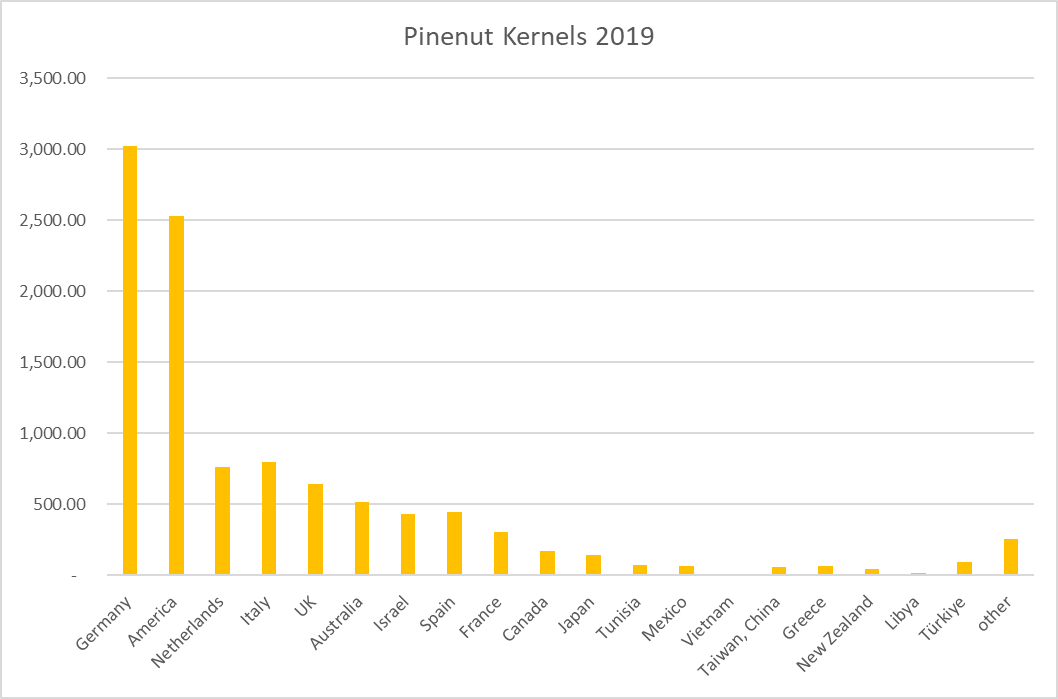

4. Comparative Analysis with Historical Data (Pre-2022)

(A) EU’s Erosion

- Germany’s share declined to 29.8% (2022) from 27.1% (2016), while Italy’s fell to 6.9% (from 5.5% in 2016).

- Spain grew modestly (+4.1% CAGR) as processors favored over Pakistani supplies.

(B) U.S. Protectionism

- Tariffs reduced to the U.S. by **-27.6%** (2016–2022), despite 2021’s partial recovery.

(C) MENA Volatility

- Israel’s imports fluctuated between 314–744 MT (2016–2022), while Tunisia collapsed to 26 MT (from 297 MT in 2016).